Middle East Ultra-High-Net-Worth Individuals (UHNWIs) Lifestyle Consumption Index 2025

Issued by: Pridebay Asia

Executive Summary

The 2025 Pridebay Asia Middle East UHNWI Lifestyle Consumption Index registers at 112.47, representing a 12.47% year-on-year growth from 2024. This robust expansion reflects the region’s resilient wealth ecosystem, policy-driven economic diversification, and UHNWIs’ unwavering demand for exclusive, value-aligned lifestyle experiences.

Key findings:

- Luxury Goods (30% index weight) leads with 7.5% YoY growth, fueled by a GCC luxury market projected to reach US$37.6 billion by 2033 .

- High-End Real Estate (25% weight) surges 18% YoY, driven by record-breaking transactions (e.g., Dubai’s US$116 million Emirates Hills villa) and 9,800 millionaires relocating to the UAE in 2025 .

- Premium Travel & Mobility (20% weight) grows 16.1% YoY, supported by 15% higher private jet traffic in Dubai and a US$980 billion Middle East tourism market .

- Alternative Investments (15% weight) rises 10% YoY, with MENA art auctions and equestrian assets remaining core to UHNW portfolios.

- Lifestyle Services (10% weight) expands 8% YoY, driven by luxury dining, medical tourism, and wellness consumption.

The UAE (118.2) and Saudi Arabia (110.5) emerge as top-performing markets, while cross-border consumption links with Asia—particularly Chinese luxury tourism and real estate investment—strengthens. For Asian HNWIs, the index highlights opportunities in co-investment in luxury real estate, partnerships in sustainable luxury, and access to exclusive regional experiences.

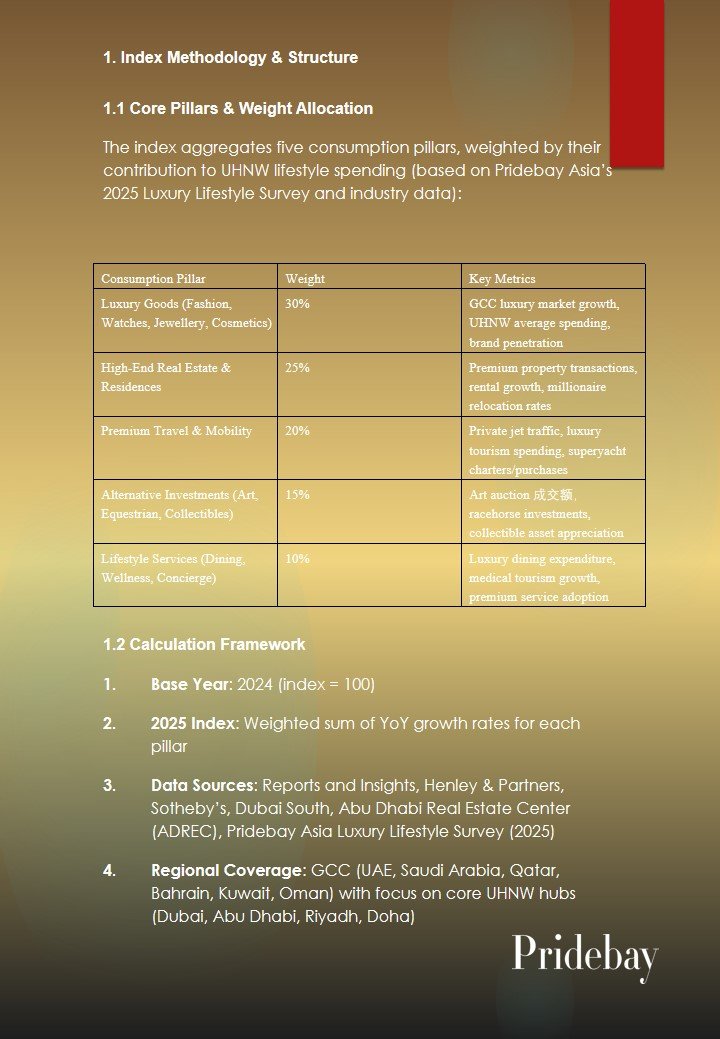

1. Index Methodology & Structure

1.1 Core Pillars & Weight Allocation

The index aggregates five consumption pillars, weighted by their contribution to UHNW lifestyle spending (based on Pridebay Asia’s 2025 Luxury Lifestyle Survey and industry data):

|

Consumption Pillar |

Weight |

Key Metrics |

|

Luxury Goods (Fashion, Watches, Jewellery, Cosmetics) |

30% |

GCC luxury market growth, UHNW average spending, brand penetration |

|

High-End Real Estate & Residences |

25% |

Premium property transactions, rental growth, millionaire relocation rates |

|

Premium Travel & Mobility |

20% |

Private jet traffic, luxury tourism spending, superyacht charters/purchases |

|

Alternative Investments (Art, Equestrian, Collectibles) |

15% |

Art auction 成交额,racehorse investments, collectible asset appreciation |

|

Lifestyle Services (Dining, Wellness, Concierge) |

10% |

Luxury dining expenditure, medical tourism growth, premium service adoption |

1.2 Calculation Framework

- Base Year: 2024 (index = 100)

- 2025 Index: Weighted sum of YoY growth rates for each pillar

- Data Sources: Reports and Insights, Henley & Partners, Sotheby’s, Dubai South, Abu Dhabi Real Estate Center (ADREC), Pridebay Asia Luxury Lifestyle Survey (2025)

- Regional Coverage: GCC (UAE, Saudi Arabia, Qatar, Bahrain, Kuwait, Oman) with focus on core UHNW hubs (Dubai, Abu Dhabi, Riyadh, Doha)

2. 2025 Index Performance by Pillar

2.1 Luxury Goods (Index: 107.5 | YoY +7.5%)

The GCC luxury goods market, valued at US6 billion in 2024, grows 7.5% in 2025, driven by rising disposable income (Saudi Arabia’s disposable income reaches US0.51 trillion) and global brand expansion . Key trends:

- UHNW average annual luxury spending exceeds US$12,000, with watches/jewellery (35% of spending) and modest luxury fashion (28%) leading .

- Online luxury sales account for 25% of transactions, with platforms like Farfetch and Ounass gaining traction.

- Sustainable luxury adoption rises 47% among GCC UHNWIs, with brands like Hermès and local label Bouguessa expanding eco-friendly collections.

2.2 High-End Real Estate (Index: 118.0 | YoY +18.0%)

The sector posts the strongest growth, fueled by investor-friendly policies and supply-demand imbalance:

- Abu Dhabi’s luxury real estate transactions surge 42% YoY in H1 2025, with apartment prices up 14% and villas 11% .

- Dubai records landmark sales: a US116 million Emirates Hills villa and US82 million Palm Jumeirah beachfront property .

- 68% of global HNWIs express interest in Dubai real estate, with Saudi and Indian investors leading demand .

- Rental markets strengthen: Abu Dhabi’s luxury rental growth hits 6% YoY, with apartments up 21% in two years .

2.3 Premium Travel & Mobility (Index: 116.1 | YoY +16.1%)

Mobility and travel remain cornerstones of UHNW lifestyle:

- Private jet traffic at Dubai South’s Mohammed bin Rashid Aerospace Hub rises 15% YoY (9,753 movements in H1 2025) .

- Middle East tourism reaches US980 billion in 2025, with UHNW客单价 (average spending) doubling the global average at US150 .

- Superyacht charters during high-profile events (Abu Dhabi Grand Prix) command 300% premiums, with 60+ meter vessels renting for US$1.5-2 million/week .

- Chinese luxury tourism to the Middle East grows 800% vs. 2019, with custom tours averaging US$50,000/person .

2.4 Alternative Investments (Index: 110.0 | YoY +10.0%)

Cultural and experiential investments gain momentum:

- MENA art auctions see strong demand: Sotheby’s 2025 London sales feature works by Shafic Abboud and Fahrelnissa Zeid with estimates up to US$138,000 .

- Equestrian investments grow 12.5% YoY, with the GCC equestrian market valued at US$4.2 billion and top racehorses fetching seven-figure sums .

- Collectibles (vintage luxury, equestrian memorabilia) appreciate 8-12% annually, with UHNWIs allocating 3-7% of portfolios to these assets.

2.5 Lifestyle Services (Index: 108.0 | YoY +8.0%)

Premium services cater to UHNW demand for convenience and exclusivity:

- Luxury dining expenditure rises 9% YoY, with Dubai and Abu Dhabi’s Michelin-starred restaurants reporting 85% occupancy rates .

- Medical tourism grows 15% YoY, with Abu Dhabi’s 高端医疗中心 (premium medical centers) hosting 500,000+ international patients (average spending US$20,000) .

- Concierge services (private styling, event planning) see 7% growth, with UHNWIs spending US$20,000+ annually on race-day and event-related services.

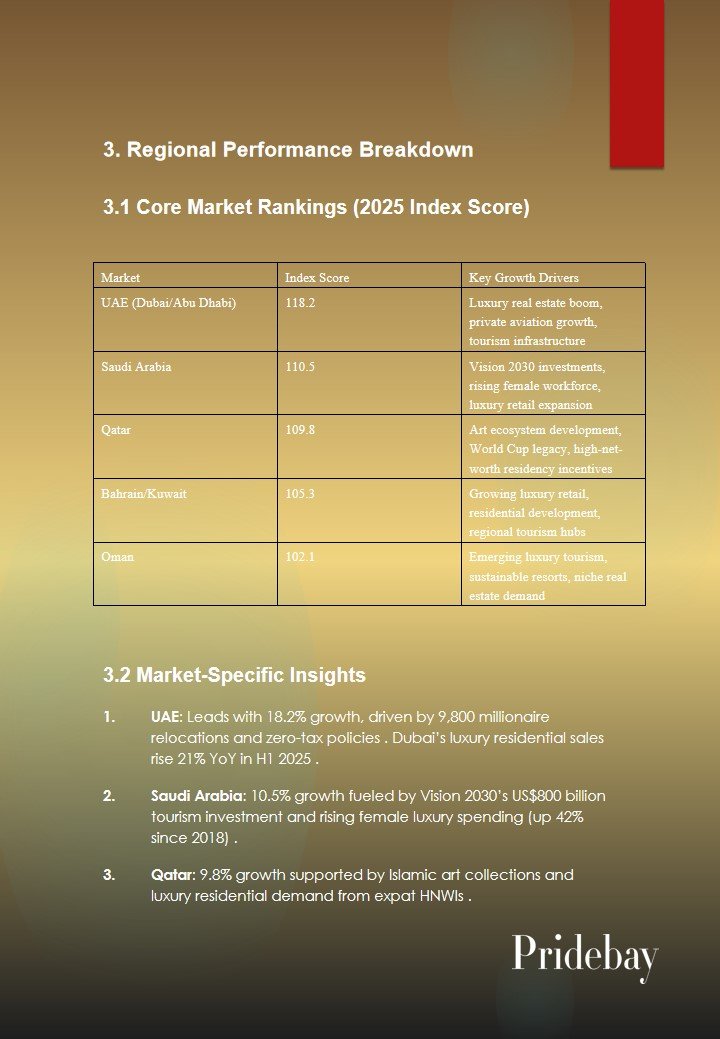

3. Regional Performance Breakdown

3.1 Core Market Rankings (2025 Index Score)

|

Market |

Index Score |

Key Growth Drivers |

|

UAE (Dubai/Abu Dhabi) |

118.2 |

Luxury real estate boom, private aviation growth, tourism infrastructure |

|

Saudi Arabia |

110.5 |

Vision 2030 investments, rising female workforce, luxury retail expansion |

|

Qatar |

109.8 |

Art ecosystem development, World Cup legacy, high-net-worth residency incentives |

|

Bahrain/Kuwait |

105.3 |

Growing luxury retail, residential development, regional tourism hubs |

|

Oman |

102.1 |

Emerging luxury tourism, sustainable resorts, niche real estate demand |

3.2 Market-Specific Insights

- UAE: Leads with 18.2% growth, driven by 9,800 millionaire relocations and zero-tax policies . Dubai’s luxury residential sales rise 21% YoY in H1 2025 .

- Saudi Arabia: 10.5% growth fueled by Vision 2030’s US$800 billion tourism investment and rising female luxury spending (up 42% since 2018) .

- Qatar: 9.8% growth supported by Islamic art collections and luxury residential demand from expat HNWIs .

4. Key Trends Shaping the Index

4.1 Policy-Driven Consumption

- UAE’s Golden Visa program (offering residency for 40+ meter yacht owners and luxury property buyers) drives 45% YoY growth in high-value asset acquisitions .

- Saudi Arabia’s labor reforms (equal pay, female workforce expansion) boost disposable income, with women now accounting for 24% of family luxury spending .

4.2 Sustainable & Purpose-Driven Spending

- 47% of GCC UHNWIs prioritize sustainability in luxury purchases, driving demand for eco-friendly yachts, solar-powered residences, and ethical fashion .

- ESG-aligned assets (sustainable real estate, green art) grow 15% faster than traditional luxury categories.

4.3 Asia-Middle East Cross-Border Linkages

- Chinese HNWIs invest US$2.3 billion in UAE luxury real estate in 2025, with Palm Jumeirah and Emirates Hills as top targets .

- Asian luxury brands (e.g., Huaxizi, Faraday Future) expand in the GCC, adapting products to regional preferences (halal beauty, modest fashion) .

- Middle Eastern UHNWIs increasingly cruise to Asian destinations (Maldives, Thailand), with 25% of 2025 superyacht itineraries including Southeast Asia .

4.4 Digital Transformation

- 85% of UHNWIs research luxury purchases online (social media, brand websites), while 25% complete transactions digitally .

- Virtual viewings (real estate, art auctions) and AI-powered personal shopping services boost engagement, particularly among younger UHNWIs (under 40).

5. Investment & Collaboration Opportunities for Asian HNWIs

5.1 Core Opportunities

- Luxury Real Estate Co-Investment: Partner with regional developers on premium projects in Dubai and Abu Dhabi, leveraging 14-18% annual price appreciation .

- Sustainable Luxury Partnerships: Collaborate with Middle Eastern brands on eco-friendly products (e.g., solar-powered yachts, organic beauty) to tap 47% growth in sustainable spending .

- Exclusive Experience Access: Curate cross-border lifestyle packages (private jet tours, art auction previews, equestrian events) for Asian HNWIs seeking regional exclusivity.

- Alternative Asset Allocation: Invest in MENA art and equestrian assets, which outperform global alternatives with 10-12% annual returns .

5.2 Risk Mitigation

- Prioritize markets with stable regulatory frameworks (UAE, Qatar) to avoid policy volatility.

- Align with cultural preferences (modest luxury, halal services) to enhance market penetration.

- Leverage local partnerships (e.g., Pridebay Asia’s regional network) for on-the-ground insights and access.

6. Future Outlook (2026 Projection)

The 2026 index is projected to reach 125.8 (11.8% YoY growth), driven by:

- Saudi Arabia’s NEOM luxury development and Red Sea Project (US$500 billion investment) .

- UAE’s expansion of Golden Visa incentives to include smaller luxury assets (30+ meter yachts, US$5 million+ real estate) .

- Growth in cross-border Asian-Middle Eastern luxury tourism and investment (projected 20% YoY increase) .

Key risks include global economic volatility and supply chain constraints for luxury goods, though the GCC’s tax-free environment and sovereign wealth fund support will mitigate these factors.

Data Sources: Reports and Insights (2025), Henley & Partners (2025), Sotheby’s (2025), Dubai South (2025), Abu Dhabi Real Estate Center (ADREC, 2025), Middle East Monitor (2025), UAE Stories (2025), Pridebay Asia Luxury Lifestyle Survey (2025).