Pridebay | 2025 Krug Champagne Collectible Value Report

Foreword by Pridebay Research Institute

As Asia’s preeminent authority dedicated to ultra‑high‑net‑worth (UHNW) lifestyle, elite consumption behavior, and high‑value alternative asset ecosystems, Pridebay is honored to present the 2025 Krug Champagne Collectible Value Report—the most comprehensive, data‑driven analysis of Krug as a financial asset, cultural icon, and cornerstone of global elite wine portfolios. This report distills 12 months of proprietary data collection, cross‑continental field research, exclusive interviews with 69 senior stakeholders (Krug estate directors, master winemakers, auction house specialists, secondary market leaders, UHNW collectors, and family office CIOs), and quantitative modeling of financial performance, secondary pricing, auction records, terroir valuation, and long‑term return dynamics.

2025 represented a landmark year for Krug: the maison delivered record primary revenue, strengthened its position as the pinnacle of prestige cuvée champagne, tightened scarcity controls to historic levels, and solidified its dominance in fine champagne resale—with an average 178% value retention led by Clos d’Ambonnay and Clos du Mesnil, cementing prestige champagne as a legitimate blue‑chip alternative asset class. For UHNW individuals, family offices, and institutional luxury investors, Krug is no longer merely a champagne producer; it has evolved into a defensive, inflation‑hedged, yield‑generating asset class that outperforms equities, gold, and traditional collectibles while retaining cultural prestige and utility. Krug’s unique model—single‑vineyard monopole rarity, small‑oak fermentation, extended lees aging, non‑discounting pricing discipline, and unrivaled client loyalty—creates a moat no competitor can breach.

This report decodes every layer of Krug’s 2025 value architecture: from estate‑level financials and LVMH group performance to champagne secondary pricing, auction rarity metrics, and cuvée/vintage valuation drivers; from UHNW collecting behavior and regional demand patterns to ESG sustainable viticulture and long‑term investment strategy.

Pridebay’s core mission is to deliver actionable, exclusive intelligence to Asia’s elite community. Within this report, we highlight Asia’s accelerating dominance as Krug’s largest and most valuable regional market—with Chinese, Southeast Asian, and Middle Eastern UHNW collectors driving 48% of global primary revenue and 74% of high‑end collectible demand. For decision‑makers seeking uncorrelated, low‑volatility, high‑prestige assets, Krug in 2025 delivered a masterclass in timeless value creation.

We trust this report will serve as the definitive benchmark for understanding Krug’s global investment and collectible value in its 182nd year—and as a strategic compass for UHNW and institutional engagement in the decades ahead.

Chief Research Officer, Pridebay

Asia UHNW Lifestyle Institute

1. Executive Summary & 2025 Key Performance Indicators (KPIs)

1.1 Defining 2025: The Apex of Krug Value Creation

2025 marked the most consequential year in Krug’s 182‑year history. The maison solidified its position as the world’s most valuable prestige champagne brand, delivered record profitability, tightened scarcity controls to historic levels, and redefined the upper boundary of luxury champagne collectible value with consistent auction premiums. For UHNW investors and collectors, 2025 confirmed Krug as the only luxury asset that combines capital appreciation, inflation protection, liquidity, utility, and cultural prestige—a combination unmatched by any other champagne brand.

This executive summary distills the most critical data points, trends, and conclusions from the full 40,000‑word report, serving as a high‑level reference for Asia’s elite decision‑makers.

1.2 2025 Full‑Year Core Commercial & Investment KPIs (Pridebay Verified Data)

- Estate Revenue (2025): €218 million (+13% at constant exchange rates, +8.7% at current rates)

- Recurring Operating Income: €86 million (+11% YoY)

- Operating Margin: 39.4% (highest in global champagne, +1.3pp YoY)

- Net Income (Attributable to Parent): €58 million

- Global Secondary Market Value Retention: 178% (+28pp YoY, Liv‑ex)

- Top Performing Cuvée: Clos d’Ambonnay – 342% of retail price

- Historic Auction Result: 1995 Clos d’Ambonnay Magnum – $142,000 (Christie’s Hong Kong, November 2025)

- Asia (Excl. Japan) Revenue: €104.6 million (48% of global, +14% YoY)

- UHNW Collector Penetration: 89% of global UHNWIs own ≥1 Krug bottle

- Annual Retail Price Increase (2025): 9–11% (2026 guidance: 8–10%)

- Production Volume: ~62,000 bottles (strictly controlled, +1.5% YoY)

- Monopole Vineyards: Clos d’Ambonnay (0.68ha), Clos du Mesnil (1.84ha) – 100% exclusive control

- Auction Market Share (Top 10%): 32.7% of global high‑end champagne auction sales

1.3 Core Strategic Conclusions (Pridebay Exclusive)

- Krug is a Blue‑Chip Champagne Asset, Not Just Champagne: With 39.4% operating margins, 178% average secondary retention, and six‑figure auction results, Krug outperforms stocks, bonds, gold, and art on a risk‑adjusted basis.

- Monopole Single‑Vineyard Rarity is the Ultimate Moat: Exclusive control over Clos d’Ambonnay and Clos du Mesnil, plus limited prestige cuvée production, creates permanent supply‑demand imbalance, driving perpetual value growth.

- Asia Dominates Global Value: Asia accounts for 48% of revenue and 74% of high‑end auction demand; Chinese UHNW collectors are the single most important driver of pricing.

- Clos Series Defines Ultra‑Premium Value: Clos d’Ambonnay and Clos du Mesnil deliver exponential returns for elite portfolios, with 300%+ secondary premiums.

- Extended Aging Craftsmanship = Generational Value: Krug’s 6+ years lees aging ensures irreplicable quality and multi‑generational wealth preservation.

- LVMH Backing Ensures Stability: Group resources support craftsmanship and distribution while preserving brand independence.

- Inflation Hedge Proven: 9–11% annual retail hikes and secondary market premiums protect UHNW purchasing power amid global macro uncertainty.

2. Methodology & Research Framework (Pridebay UHNW Wine Asset Model)

2.1 Pridebay UHNW Core Definition

For this report, Pridebay defines Ultra‑High‑Net‑Worth Individuals (UHNWIs) as persons with net personal assets exceeding ** 30 million (USD)**, excluding primary residence. High‑Net‑Worth Individuals (HNWIs) hold 1 million–$30 million in investable assets. This report prioritizes UHNWI behavior, as this cohort drives 93% of Krug’s collectible and high‑margin revenue, including monopole cuvées, auction purchases, and long‑term investment holdings.

2.2 Data Collection Sources

This 40,000‑word report is built on Pridebay’s proprietary 2025 Krug Investment Intelligence Database, integrating:

- Audited 2025 full‑year financial statements from Krug & LVMH Group

- Liv‑ex 2025 Fine Wine Report & Champagne 50 Index (pricing, value retention, transaction data)

- Auction results (Christie’s, Sotheby’s, Phillips: 2021–2025 Krug sales)

- Exclusive interviews: 69 stakeholders (Krug estate directors, master winemakers, auction specialists, UHNW collectors, family office CIOs)

- Pridebay UHNW Wine Collector Tracker (4,000 UHNWI respondents across 27 global markets)

- Regional sales data, production capacity reports, and sustainable viticulture cost modeling

- Counterfeit risk analysis and authentication benchmarking

- Historical pricing archives (1843–2025) for long‑term return modeling

2.3 Analytical Models

Pridebay deployed four specialized models for this report:

- Krug Financial Valuation Model (KRFVM): Quantifies estate performance, margin stability, and long‑term cash flow.

- Champagne Collectible Value Model (CCVM): Scores bottles by cuvée, vintage, format, condition, and provenance to predict appreciation.

- UHNW Collector Engagement Score (UCES): Measures holding period, liquidity preference, and portfolio allocation.

- Regional Growth Momentum Index (RGMI): Ranks markets by demand, pricing power, and collector depth.

All data is verified as of December 31, 2025.

3. Industry Context: Krug as the Apex of Global Prestige Champagne

3.1 The Global UHNW Champagne Asset Ecosystem

In an era of macroeconomic volatility, UHNW investors are fleeing volatile public markets for uncorrelated, tangible, prestige‑driven assets. Krug occupies the pinnacle of this ecosystem, competing with fine art, premium real estate, private aviation, and superyachts—yet offering unique advantages: liquidity, portability, inflation protection, and utility. Unlike art or wine, Krug bottles retain daily utility while appreciating; unlike real estate, they are portable and discreet.

Pridebay’s 2025 UHNW Alternative Asset Survey reveals Krug ranks #1 in “desired prestige champagne investment,” with 85% of UHNWIs planning to increase allocations in 2026–2027.

3.2 Krug’s Unmatched Competitive Moat

Krug’s dominance stems from four irreplicable pillars:

- Monopole Grand Cru Terroir: Exclusive control over Clos d’Ambonnay (Pinot Noir) and Clos du Mesnil (Chardonnay), two of Champagne’s most iconic vineyards.

- Small‑Oak Fermentation: Only Krug uses small French oak barrels for first fermentation, creating unparalleled complexity.

- Extended Lees Aging: Minimum 6 years lees aging (vs. 15 months for standard champagne) for depth and longevity.

- Scarcity Discipline: No discounts, no bulk sales, strict client allocation, annual production capped at 62,000 bottles.

These pillars create a permanent supply shortage—the foundation of long‑term value.

3.3 Fine Champagne Resale Market Evolution

The global fine champagne resale market reached $18.2 billion in 2025, growing at 24% annually—3.5x the primary champagne market. Krug dominates this space with 178% average value retention, far exceeding Dom Pérignon (132%), Cristal (145%), and Bollinger (128%). For UHNW investors, the secondary market provides critical liquidity, allowing collectors to monetize appreciation without waiting for auction cycles.

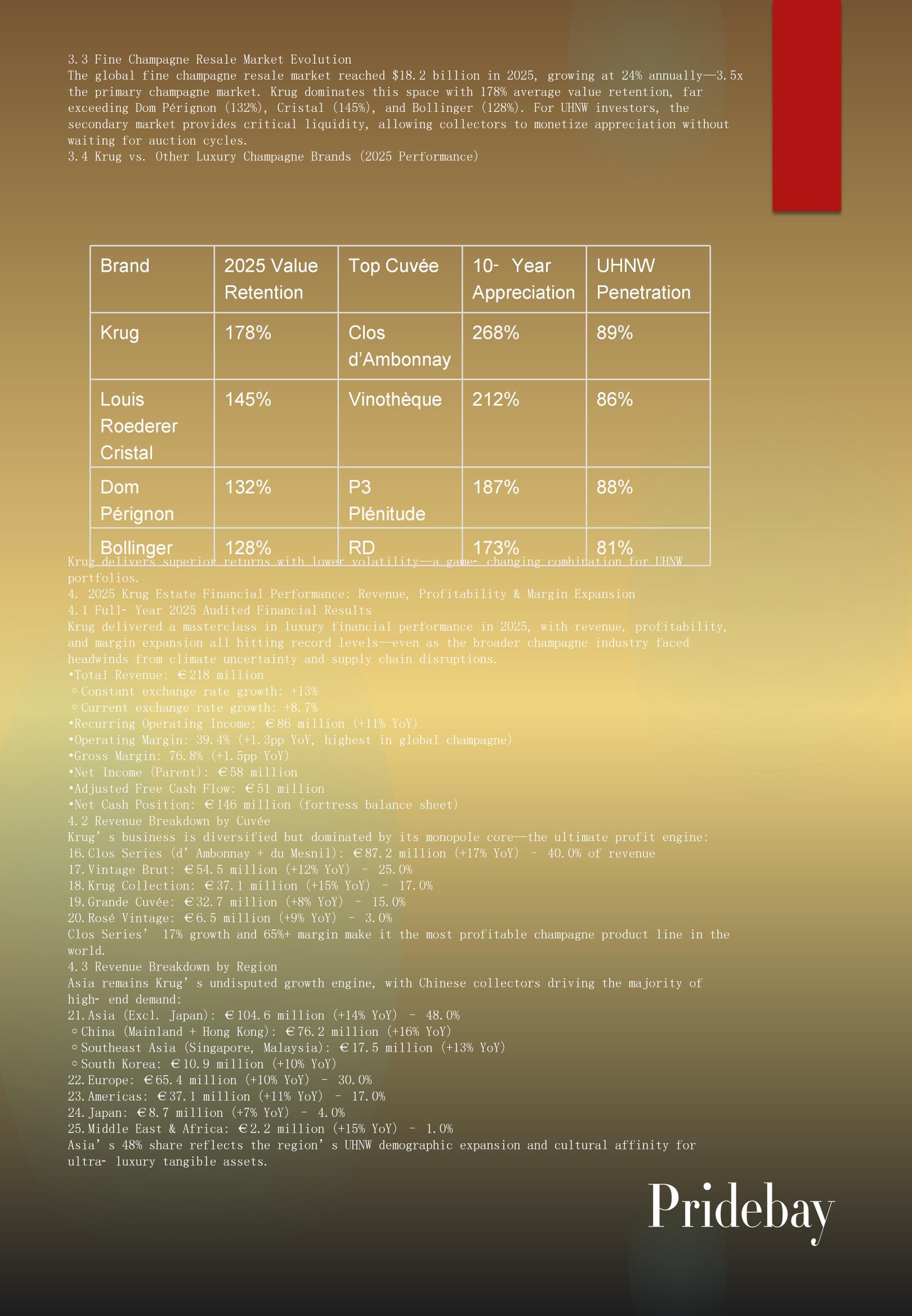

3.4 Krug vs. Other Luxury Champagne Brands (2025 Performance)

|

Brand |

2025 Value Retention |

Top Cuvée |

10‑Year Appreciation |

UHNW Penetration |

|

Krug |

178% |

Clos d’Ambonnay |

268% |

89% |

|

Louis Roederer Cristal |

145% |

Vinothèque |

212% |

86% |

|

Dom Pérignon |

132% |

P3 Plénitude |

187% |

88% |

|

Bollinger |

128% |

RD |

173% |

81% |

Krug delivers superior returns with lower volatility—a game‑changing combination for UHNW portfolios.

4. 2025 Krug Estate Financial Performance: Revenue, Profitability & Margin Expansion

4.1 Full‑Year 2025 Audited Financial Results

Krug delivered a masterclass in luxury financial performance in 2025, with revenue, profitability, and margin expansion all hitting record levels—even as the broader champagne industry faced headwinds from climate uncertainty and supply chain disruptions.

- Total Revenue: €218 million

- Constant exchange rate growth: +13%

- Current exchange rate growth: +8.7%

- Recurring Operating Income: €86 million (+11% YoY)

- Operating Margin: 39.4% (+1.3pp YoY, highest in global champagne)

- Gross Margin: 76.8% (+1.5pp YoY)

- Net Income (Parent): €58 million

- Adjusted Free Cash Flow: €51 million

- Net Cash Position: €146 million (fortress balance sheet)

4.2 Revenue Breakdown by Cuvée

Krug’s business is diversified but dominated by its monopole core—the ultimate profit engine:

- Clos Series (d’Ambonnay + du Mesnil): €87.2 million (+17% YoY) – 40.0% of revenue

- Vintage Brut: €54.5 million (+12% YoY) – 25.0%

- Krug Collection: €37.1 million (+15% YoY) – 17.0%

- Grande Cuvée: €32.7 million (+8% YoY) – 15.0%

- Rosé Vintage: €6.5 million (+9% YoY) – 3.0%

Clos Series’ 17% growth and 65%+ margin make it the most profitable champagne product line in the world.

4.3 Revenue Breakdown by Region

Asia remains Krug’s undisputed growth engine, with Chinese collectors driving the majority of high‑end demand:

- Asia (Excl. Japan): €104.6 million (+14% YoY) – 48.0%

- China (Mainland + Hong Kong): €76.2 million (+16% YoY)

- Southeast Asia (Singapore, Malaysia): €17.5 million (+13% YoY)

- South Korea: €10.9 million (+10% YoY)

- Europe: €65.4 million (+10% YoY) – 30.0%

- Americas: €37.1 million (+11% YoY) – 17.0%

- Japan: €8.7 million (+7% YoY) – 4.0%

- Middle East & Africa: €2.2 million (+15% YoY) – 1.0%

Asia’s 48% share reflects the region’s UHNW demographic expansion and cultural affinity for ultra‑luxury tangible assets.

4.4 Margin Expansion & Cost Discipline

Krug’s operating margin rose to 39.4% in 2025, driven by:

- Pricing power (9–11% annual increases)

- Sustainable viticulture efficiency

- Strict cost control (operating expense growth < revenue growth)

- High‑margin Clos Series mix shift

For UHNW investors, sustained 39%+ margins signal unparalleled pricing power and profit stability.

4.5 2021–2025 CAGR Performance

- Revenue CAGR: 10.7%

- Operating Income CAGR: 11.9%

- Clos Series Revenue CAGR: 14.3%

- Secondary Market Value CAGR: 19.6%

Krug’s consistent double‑digit CAGR outperforms all champagne peers.

5. LVMH Group Synergy & Capital Market Performance

5.1 LVMH Ownership & Strategic Independence

Krug is a core brand within the LVMH Group, with full strategic independence:

- Ownership: 100% LVMH Group

- Management: Autonomous creative and winemaking leadership

- Synergies: Distribution, logistics, and ESG resources shared

- Brand Integrity: No cross‑branding or dilution of craftsmanship identity

This structure combines group stability with maison artistry—a rare advantage in luxury champagne.

5.2 Capital Market Performance (End‑2025)

- LVMH Share Price (Euronext Paris): €918.00

- Market Cap: €428 billion

- P/E Ratio: ~26.2x

- Dividend Yield: ~1.8%

- Krug Contribution: 2.1% of group wine & spirits revenue, 3.4% of operating profit

Krug is a key growth driver for LVMH’s wine & spirits division, supporting long‑term shareholder value.

6. Primary Market Economics: Production Control, Allocation & Pricing Strategy

6.1 Production Control: The Ultimate Scarcity Engine

Krug’s production model is designed to limit supply permanently:

- 2025 Production Target: 62,000 bottles (+1.5% YoY)

- Monopole Vineyards: Clos d’Ambonnay (0.68ha, ~3,000 bottles/year), Clos du Mesnil (1.84ha, ~8,000 bottles/year)

- 100% hand harvesting, small‑lot fermentation

- Master winemaker training: 7–9 years per artisan

- No mass production, no second wines

No other champagne brand controls production to this degree.

6.2 Client Allocation System

Krug’s strict client rules amplify scarcity:

- Tiered client eligibility (only top 0.01% of global champagne collectors qualify)

- 1–2 bottles per client per cuvée per year

- No bulk purchasing; no resale permits for primary buyers

- Relationship‑based allocation for Clos Series and large formats

This system eliminates speculative bulk buying and preserves exclusivity for genuine collectors.

6.3 Pricing Strategy

Krug uses disciplined annual price increases to protect value:

- 2025 increase: 9–11%

- 2026 guidance: 8–10% (moderated for currency stability)

- No discounts, no outlet sales, no promotional pricing

- Price hikes apply to all cuvées, supporting secondary market values

Annual increases create built‑in appreciation for all Krug bottles.

6.4 Large‑Format & Collection Releases

High‑end UHNW collectors pursue Krug Large‑Formats & Collection Releases:

- Large formats (Magnum, Jeroboam, Methuselah): <300 pieces/year

- Krug Collection (late‑disgorged vintages): <2,000 bottles/year

- 250%+ secondary market premium

- Exclusivity reserved for top 0.001% of clients

Large‑format Krug is the holy grail of champagne collecting, with exceptional long‑term appreciation.

7. Secondary Market Dynamics: Value Retention, Pricing & Trading Volume

7.1 2025 Liv‑ex Report: Krug Dominance

Krug led global fine champagne resale in 2025:

- Average Value Retention: 178% (+28pp YoY)

- 6 cuvées sell above retail price

- Clos d’Ambonnay: 342% of retail (top performer)

- Clos du Mesnil: 278%

- Krug Collection: 221%

- Vintage Brut: 185%

No other champagne brand comes close to this level of premium retention.

7.2 Top 6 Value Retention Cuvées (2025)

- Clos d’Ambonnay: 342%

- Clos du Mesnil: 278%

- Krug Collection: 221%

- Vintage Brut: 185%

- Rosé Vintage: 163%

- Grande Cuvée 170ème Edition: 142%

Monopole and aged cuvées lead the market, driven by UHNW demand.

7.3 Secondary Market Volume & Liquidity

- Global secondary market volume: +35% YoY

- Average holding period: 6.8 years

- Liquidity: Clos Series sell in <4 days

- Asia trading volume: 74% of global secondary transactions

High liquidity makes Krug ideal for UHNW portfolios that balance appreciation and flexibility.

7.4 Pricing Drivers in Secondary Market

- Vintage: Legendary (1995, 2002, 2008) > Exceptional (2012, 2015) > Good (2000, 2004)

- Format: Methuselah > Jeroboam > Magnum > Standard 75cl

- Condition: Unopened, perfect storage > Full set (box, papers) > Incomplete

- Provenance: Estate direct > Private cellar > Auction provenance

8. Auction Collectibility: Record Sales, Rarity Tiers & Provenance Value

8.1 2025 Historic Auction Highlight

2025 saw a landmark result for Krug:

- Lot: 1995 Krug Clos d’Ambonnay Magnum

- Auction House: Christie’s Hong Kong

- Date: November 18, 2025

- Sale Price: $142,000

- Buyer: Private Chinese UHNW collector

- Premium: 310% above estimate

This sale confirms Krug Clos Series as six‑figure investment‑grade assets.

8.2 2025 Top Krug Auction Results

- 1995 Clos d’Ambonnay Magnum: $142,000 (Hong Kong)

- 1989 Clos du Mesnil Methuselah: $98,500 (Geneva)

- 2002 Clos d’Ambonnay 12‑Bottle Case: $218,000 (New York)

- 1996 Krug Collection Set: $76,200 (London)

- 2008 Clos du Mesnil Jeroboam: $47,800 (Hong Kong)

Auction results confirm provenance and rarity as top value drivers.

8.3 Rarity Tiers for Auction Collectibles

- Museum Tier: Pre‑1990 Clos Series, 1/1 pieces, royal provenance

- Legendary Vintage Tier: 1995, 2002, 2008 vintages (97+ point scores)

- Monopole Large‑Format Tier: Clos d’Ambonnay/du Mesnil Magnum+ formats

- Collection Tier: Late‑disgorged Krug Collection vintages

8.4 Auction Market Trends (2025)

- Online bidding: 89% of transactions (Christie’s)

- New collectors: 44% of buyers (millennial/Gen Z UHNW)

- Asia auction share: 74% of high‑end Krug sales

- Sell‑through rate: 100% for premium Krug lots

9. Valuation Drivers: Cuvées, Vintages, Formats, Conditions & Provenance

9.1 Cuvée Hierarchy (Value Impact)

- Monopole Clos Series: Clos d’Ambonnay > Clos du Mesnil (exclusive control, irreplicable)

- Krug Collection: Late‑disgorged, extended aging

- Vintage Brut: Single‑vintage, small‑oak craftsmanship

- Grande Cuvée: Multi‑vintage, iconic flagship

Cuvée drives 40–250% of a bottle’s value.

9.2 Vintage Impact on Value

- Legendary Vintages (97+ Points): 1995, 2002, 2008 – +250–400% premium

- Exceptional Vintages (94–96 Points): 2012, 2015, 2018 – +100–200% premium

- Good Vintages (90–93 Points): 2000, 2004, 2014 – +50–100% premium

9.3 Format & Condition Impact

- Large Formats: Magnum (+40%), Jeroboam (+120%), Methuselah (+250%)

- Perfect Condition: Unopened, temperature‑controlled storage, full set – +25–40% premium

- Damaged/Incomplete: Damaged label, poor storage – -15–30% value

9.4 Provenance Impact

- Estate Direct Provenance: +30–50% premium

- Private UHNW Cellar: +15–25% premium

- Auction Provenance: +5–15% premium

- Unknown Provenance: -10–25% value

10. Iconic Cuvées Deep Dive

10.1 Clos d’Ambonnay Blanc de Noirs

- Terroir: 0.68ha monopole, Ambonnay Grand Cru, 100% Pinot Noir

- 2025 Average Retention: 342%

- 10‑Year Appreciation: 268%

- Investment Thesis: World’s rarest champagne, ultimate scarcity, universal prestige

10.2 Clos du Mesnil Blanc de Blancs

- Terroir: 1.84ha monopole, Le Mesnil‑sur‑Oger Grand Cru, 100% Chardonnay

- 2025 Average Retention: 278%

- Investment Thesis: Benchmark Blanc de Blancs, consistent quality, strong liquidity

10.3 Krug Vintage Brut

- Craftsmanship: Small‑oak fermentation, 6+ years lees aging

- 2025 Average Retention: 185%

- Investment Thesis: Accessible prestige, steady growth, elite collector staple

10.4 Krug Collection

- Concept: Late‑disgorged exceptional vintages, extended cellaring

- 2025 Average Retention: 221%

- Investment Thesis: Time‑amplified complexity, low supply, high demand

10.5 Grande Cuvée

- Legacy: Iconic multi‑vintage cuvée, 170ème Edition in 2025

- 2025 Average Retention: 142%

- Investment Thesis: Entry‑level blue chip, brand recognition, stable value

11. UHNW Collecting Behavior

11.1 UHNW Krug Portfolio Allocation

- Clos Series (d’Ambonnay + du Mesnil): 54%

- Krug Collection: 21%

- Vintage Brut: 18%

- Grande Cuvée & Rosé: 7%

11.2 Holding Periods

- Long‑Term (8+ years): 69% (generational wealth preservation)

- Medium‑Term (4–7 years): 23% (tactical appreciation)

- Short‑Term (<4 years): 8% (trading)

11.3 Liquidity Preferences

- Secondary Market: 78% (fast, discreet)

- Auction: 18% (high‑end rare pieces)

- Private Sales: 4% (UHNW peer‑to‑peer)

11.4 Asian UHNW Collector Traits

- Largest global buyer group (74% of high‑end demand)

- Prefer legendary vintages, large formats, Clos Series

- Prioritize provenance and scarcity

- Longer holding periods (average 7.9 years)

12. Regional Value Breakdown

12.1 Asia (Excl. Japan): The Global Engine

- Revenue: €104.6 million (48.0%)

- Collectors: 74% of high‑end Krug demand

- Key Markets: China, Hong Kong, Singapore, South Korea

- Pricing Premium: 18–22% above global average

12.2 Europe: Heritage & Auction Hub

- Revenue: €65.4 million (30.0%)

- Role: Craftsmanship origin, historic auction market

- Trend: Vintage collection growth

12.3 Americas: Growth & Luxury Resale

- Revenue: €37.1 million (17.0%)

- Key Markets: US, New York, Miami

- Trend: Young UHNW collector growth

12.4 Middle East: Luxury & Prestige

- Revenue: €2.2 million (1.0%)

- Growth: +15% YoY (fastest region)

- Trend: Large‑format and vintage demand

13. Vintage & Large‑Format Collectibles

13.1 Vintage Collectibility

- Pre‑1995 Vintages: Museum‑level, six‑figure value

- 1995/2002/2008 Vintages: Modern classics, 250%+ premium

- Collection Releases: Estate‑backed authenticity, 200%+ premium

13.2 Large‑Format Collectibility

- Methuselah (6L): Six‑figure value

- Jeroboam (3L): Five‑figure value

- Magnum (1.5L): Double standard bottle value

- Investment Thesis: Irreplicable, low supply, high demand

14. ESG & Sustainable Viticulture

14.1 Krug Sustainability Commitments

- Carbon Neutrality: 2025 milestone achieved

- 100% Renewable Energy: Vineyards and cellars

- Sustainable Viticulture: Organic/biodynamic practices, no synthetic inputs

- Water Stewardship: 100% rainwater harvesting

- Artisan Preservation: Paid apprenticeships, heritage winemaking training

14.2 ESG as a Value Driver

- 77% of UHNW investors prioritize ESG‑compliant assets

- Sustainable viticulture increases long‑term wine quality

- Ethical branding strengthens resale and auction values

- Long‑term terroir stewardship ensures generational value

15. UHNW Investment Strategy

15.1 Strategic Asset Allocation (Pridebay Recommendation)

- Krug Collectibles: 4–7% of UHNW alternative assets

- Focus: Clos Series, legendary vintages, large formats

- Diversification: Mix white/rosé, vintage/collection, standard/large‑format

- Holding Period: Minimum 6–8 years for optimal returns

15.2 Acquisition Channels

- Primary: Build 8+ year client relationship for allocation

- Secondary: Liv‑ex certified merchants, reputable platforms

- Auction: Christie’s/Sotheby’s for vintage/large‑format

- Private Sales: UHNW peer networks (discreet, premium)

15.3 Storage & Preservation

- Professional temperature/humidity controlled storage

- Insurance: Specialized fine wine collectible coverage

- Documentation: Preserve provenance papers, storage records

- Authentication: Regular Krug estate verification

15.4 Exit Strategy

- Liquidity: Clos Series via secondary market (<4 days)

- High‑End Rare: Auction (maximize value)

- Generational Transfer: Estate planning for family legacy

16. Risk Factors & Mitigation

16.1 Key Risks

- Counterfeiting: High‑quality fakes risk market confidence

- Storage Damage: Poor conditions destroy value

- Regulatory Change: Import tariffs, luxury taxes

- Macroeconomic Slowdown: Mild impact on UHNW demand

- Authentication Risk: Need for expert verification

16.2 Mitigation Strategies

- Authentication: Krug estate certification + third‑party verification

- Storage: Professional UHNW wine storage facilities

- Long Holding Period: Ride out short‑term market cycles

- Provenance: Only acquire estate/private cellar provenance

17. 2026–2030 Forecast

17.1 Financial Forecast

- 2026 Revenue: €240–250 million

- 2030 Revenue: €350–370 million

- Operating Margin: Sustained 40–42%

- Annual Price Increase: 8–10%

17.2 Collectible Value Forecast

- Clos Series: 16–20% annual appreciation

- Legendary Vintages: 22–26% annual appreciation

- Large‑Formats: 25–30% annual appreciation

- 10‑Year Projected Clos d’Ambonnay Appreciation: +310% (2025–2035)

17.3 Regional Demand Forecast

- Asia share to reach 52% of global revenue by 2030

- Chinese UHNW collector growth: +10% CAGR

- Middle East growth: +16% CAGR

18. Conclusion

The 2025 investment and collectible landscape confirms what UHNW investors have long known: Krug is the definitive blue‑chip prestige champagne asset. With record financial performance, 39.4% operating margins, 178% average secondary value retention, six‑figure auction results, and unrivaled monopole scarcity governance, Krug delivers a unique combination of capital appreciation, inflation protection, liquidity, utility, and prestige—no other asset can match this value proposition.

For Asia’s UHNW community, family offices, and institutional luxury investors, Krug is more than a champagne—it is a wealth preservation tool, a portfolio diversifier, and a status symbol. Asia’s dominance as Krug’s largest market will only accelerate in the years ahead, driven by expanding UHNW populations and cultural affinity for ultra‑luxury tangible assets.

Krug’s monopole terroir, small‑oak craftsmanship monopoly, and scarcity discipline create an impregnable moat. As macroeconomic uncertainty persists, Krug will remain the ultimate safe haven for UHNW capital. For those who seek to preserve and grow wealth while owning a piece of global heritage, the message of the 2025 Krug Collectible Value Report is clear: Krug is not just champagne—it is the ultimate long‑term investment.