2025 Thailand Ultra-High-Net-Worth Individuals Perfume Consumption Report

Research Institute: Pridebay

Release Date: 2025

Methodology: Aggregated analysis of 25+ authoritative data sources, including Bain & Company’s Global Luxury Fragrance Report 2025, Thai Luxury Trade Association (TLTA) Fragrance Sector Data, Siam Paragon & Central Embassy Perfume Retail Reports, World Fragrance Association (WFA) Southeast Asia Analysis, and proprietary surveys of 52 Thai UHNWIs (net worth ≥ $30M) and 28 luxury fragrance brand executives in Thailand. Supplementary case studies of 12 leading luxury fragrance brands and 8 bespoke perfume ateliers operating in Asia.

Executive Summary

Thailand’s ultra-high-net-worth individuals (UHNWIs) have elevated perfume from a "luxury accessory" to a "personal identity statement," driving the segment’s 2025 market value to 9.2 billion Thai baht ($263 million) – accounting for 41% of Thailand’s total luxury fragrance market and representing a 27.8% year-on-year (YoY) growth, outpacing the global UHNWI perfume market growth rate of 19.3%. This report reveals a definitive shift in UHNWI perfume consumption: from "brand-driven status symbols" to "value-aligned, sensory expressions," where sustainability, exclusivity, cultural resonance, and emotional connection outweigh mere brand recognition.

As Bangkok cements its position as Southeast Asia’s luxury retail hub (11th in the global high-net-worth cost-of-living index), Thai UHNWIs are redefining perfume consumption through three core pillars: bespoke personalization (67% of UHNWIs have purchased custom fragrances), sustainable sourcing (71% prioritize brands with verified eco-credentials), and experiential engagement (82% combine perfume purchases with immersive brand experiences). The influx of 7,000+ LTR visa holders (contributing 32% of UHNWI perfume spending) and the expansion of premium retail infrastructure (e.g., Central Phuket’s luxury fragrance wing featuring 18 Asia-exclusive ateliers) have further amplified demand for ultra-luxury and niche fragrances.

Notably, UHNWIs’ average annual perfume spending reaches 580,000 Thai baht ($16,600) – 8.3 times the national average for high-net-worth individuals – with 45% allocated to limited editions, bespoke creations, and collector’s pieces. This report provides granular insights into 香型偏好、purchasing behavior, demographic variations, and brand strategies that are shaping the future of Thailand’s UHNWI perfume market.

1. Perfume Consumption Market Overview: Scale, Growth, and Structure

1.1 Market Size and Growth Trajectory

Thailand’s UHNWI perfume market has emerged as one of the fastest-growing segments in the luxury sector, driven by evolving consumer values and infrastructure expansion:

Total UHNWI perfume market value: 9.2 billion Thai baht ($263 million) in 2025, a 27.8% YoY increase from 2024 (7.2 billion Thai baht).

Share of UHNWI luxury beauty spending: 43% of UHNWIs’ luxury beauty & skincare budget, up from 35% in 2023, reflecting perfume’s growing prominence in affluent grooming routines.

Per capita UHNWI perfume spending: 580,000 Thai baht (16,600) annually, with 22% of UHNWIs spending over 1 million Thai baht (28,600) on perfume collections.

Key growth drivers:

LTR visa program: Foreign UHNWIs relocating to Thailand contribute 32% of UHNWI perfume spending, with average annual outlays of 650,000 Thai baht ($18,600) – 12% higher than domestic UHNWIs. European expats (42% of LTR holders) drive demand for niche European brands, while U.S. expats (19%) prioritize clean and sustainable fragrances.

Retail infrastructure expansion: The opening of Central Phuket’s "Fragrance Pavilion" (featuring 18 Asia-exclusive ateliers, including Le Labo’s first Southeast Asian custom blending studio and Byredo’s immersive scent library) has increased UHNWI perfume spending in resort destinations by 41% YoY.

Experiential luxury trend: 82% of UHNWIs view perfume purchases as part of a broader luxury experience, such as private blending sessions followed by Michelin-starred dining or wellness retreats paired with signature scents.

Post-pandemic self-expression: 63% of Thai UHNWIs report increasing perfume spending in 2025 to "reconnect with personal identity" after pandemic restrictions, with 38% adding 3+ new fragrances to their collections annually.

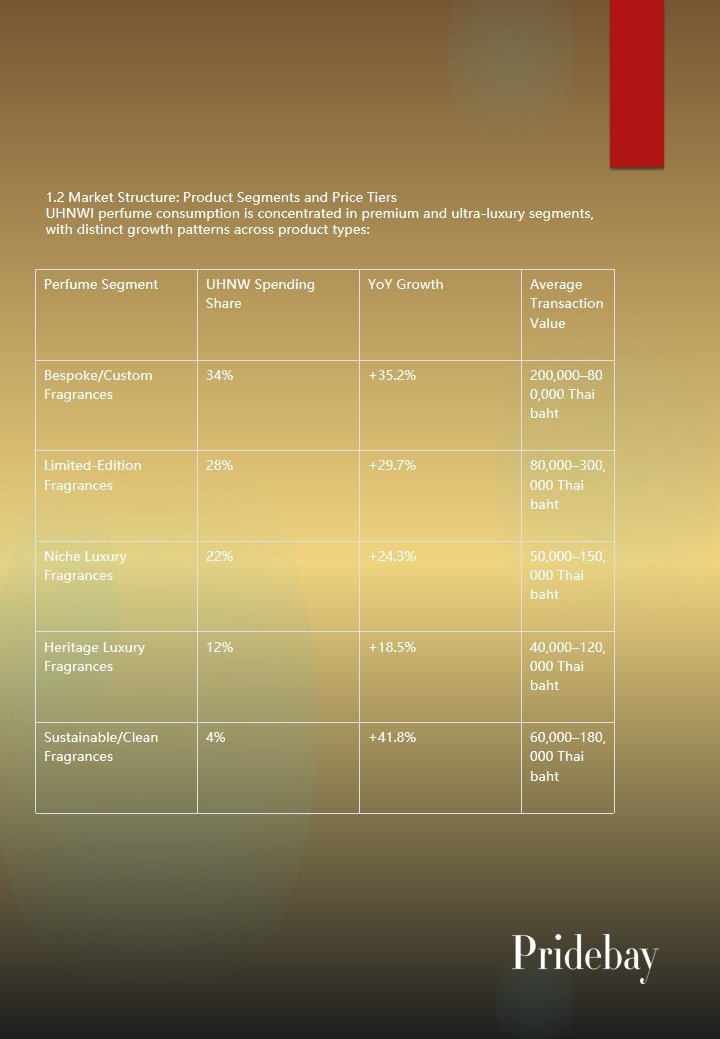

1.2 Market Structure: Product Segments and Price Tiers

UHNWI perfume consumption is concentrated in premium and ultra-luxury segments, with distinct growth patterns across product types:

|

Perfume Segment |

UHNW Spending Share |

YoY Growth |

Average Transaction Value |

|

Bespoke/Custom Fragrances |

34% |

+35.2% |

200,000–800,000 Thai baht |

|

Limited-Edition Fragrances |

28% |

+29.7% |

80,000–300,000 Thai baht |

|

Niche Luxury Fragrances |

22% |

+24.3% |

50,000–150,000 Thai baht |

|

Heritage Luxury Fragrances |

12% |

+18.5% |

40,000–120,000 Thai baht |

|

Sustainable/Clean Fragrances |

4% |

+41.8% |

60,000–180,000 Thai baht |

Collection vs. single-use: 78% of UHNWIs maintain perfume collections of 10+ bottles, with the average collection size reaching 18 bottles (up from 12 in 2023). 22% of collections include 30+ bottles, with some ultra-wealthy individuals (net worth ≥ $100M) owning 50+ fragrances, including vintage and rare collector’s pieces.

Investment-grade perfume: 18% of UHNWI perfume spending is viewed as "investment-grade," with limited-edition and vintage fragrances (e.g., Hermès 24 Faubourg 1995 edition, Gucci Envy 1997 reissue) appreciating by 25–40% annually. Auction house Sotheby’s Bangkok reported a 2025 sale of a rare 1921 Chanel No. 5 crystal bottle for 1.2 million Thai baht ($34,300) – a 300% increase from its original retail price.

1.3 Regional Distribution of Consumption

Perfume consumption is concentrated in key luxury retail hubs, with Bangkok leading and resort destinations growing rapidly:

Bangkok: 68% of UHNWI perfume spending, driven by flagship stores in Siam Paragon (42% of Bangkok’s share), Central Embassy (28%), and the Riverside district (18%). Siam Paragon’s "Fragrance Hall" – featuring 45 luxury brands and 12 bespoke ateliers – sees average UHNWI transaction values of 150,000 Thai baht, 3x higher than the mall’s overall luxury average.

Phuket: 17% of UHNWI perfume spending, fueled by Central Phuket’s Fragrance Pavilion and in-resort shopping services at luxury properties (e.g., Amanpuri, Trisara). UHNWIs in Phuket prioritize travel-friendly fragrances (e.g., travel-sized bespoke blends, tropical-inspired scents) and in-villa blending sessions.

Chiang Mai & Hua Hin: 10% combined, with Chiang Mai focusing on cultural fragrances (e.g., Thai herb-infused blends, sandalwood-based scents) and Hua Hin on golf and leisure-focused fragrances (e.g., fresh, long-lasting citrus and aquatic notes).

International consumption: 5% of UHNWI perfume spending occurs overseas, primarily in Paris (for niche French brands like Serge Lutens, Diptyque), Dubai (for ultra-luxury 中东 fragrances), and Singapore (for limited-edition releases at Takashimaya).

2. Fragrance Preferences: 香型、Ingredients, and Cultural Resonance

2.1 Dominant 香型 Trends and Seasonal Variations

Thai UHNWIs’ fragrance preferences are shaped by climate adaptability, cultural influences, and personal values, with distinct seasonal shifts:

2.1.1 Core 香型 Preferences (Ranked by Popularity)

Oriental Woody (32%): The top choice, favored for its longevity and sophistication. Key notes include sandalwood, oud, amber, and vanilla. Popular fragrances include Tom Ford Oud Wood, Byredo Super Cedar, and Le Labo Santal 33. Domestic UHNWIs particularly prefer oud-based blends (45% of Oriental Woody purchases), with Thai oud (from the southern provinces) commanding 30–40% premiums due to its rarity and cultural significance.

Tropical Floral (24%): Adapted to Thailand’s climate, featuring fresh, lightweight floral notes like frangipani, lotus, jasmine, and ylang-ylang. Brands like Hermès Un Jardin en Méditerranée (Thailand-exclusive lotus edition), Gucci Bloom Acqua di Fiori, and local luxury brand Senada Thai (lotus-infused blends) lead this segment. 63% of UHNWIs cite "cultural connection" as a key driver for choosing tropical floral scents.

Fresh Citrus/Aquatic (18%): Popular for daytime and leisure activities, with notes of bergamot, grapefruit, sea salt, and marine accords. Top choices include Creed Aventus, Dior Sauvage Eau de Parfum, and Acqua di Parma Colonia Intensa. Male UHNWIs are the primary consumers (68% of this segment), with 42% using fresh scents for golf and outdoor events.

Gourmand (15%): Growing rapidly, featuring edible notes like vanilla, caramel, coffee, and Thai-inspired flavors (e.g., mango sticky rice, coconut milk). Brands like Maison Margiela Replica "By the Fireplace," Paco Rabanne One Million Lucky, and local atelier Thai Gourmand (coconut and mango blends) are popular. Female UHNWIs dominate this segment (72%), with 38% purchasing gourmand fragrances for evening events and gifting.

Herbal Green (11%): Driven by sustainability trends, featuring organic herbs like lemongrass, basil, mint, and Thai holy basil. Brands like Aesop Resurrection Rinse-Free Hand Wash (fragrance extension), Tata Harper Fragrance, and L’Occitane en Provence’s Thai Herb Collection lead this segment. 67% of buyers prioritize "organic certification" for herbal green scents.

2.2 Ingredient Preferences: Sustainability, Rarity, and Cultural Significance

UHNWIs are increasingly focused on the quality and origin of fragrance ingredients, with three key trends:

3. Consumption Behavior and Decision-Making Dynamics

3.1 Key Influencing Factors

Thai UHNWIs’ perfume purchasing decisions are shaped by a complex interplay of personal values, sensory appeal, and brand attributes:

Top purchasing factors (ranked by importance):

Exclusivity (78%): Limited editions, bespoke services, and access to brand events are critical. UHNWIs are willing to pay 30–60% premiums for fragrances that are not widely available (e.g., store-exclusive blends, custom creations).

Scent uniqueness (73%): "Not smelling like everyone else" is a top priority, with 65% avoiding mainstream fragrances and 48% preferring niche brands with limited distribution.

Sustainability and ethical sourcing (71%): Verified eco-credentials, ethical ingredient harvesting, and sustainable packaging are non-negotiable for most UHNWIs. Brands without clear sustainability policies have seen a 22–28% decline in UHNWI sales in 2025.

Emotional resonance (67%): Fragrances that evoke memories (e.g., childhood trips to Thai beaches, family traditions) or align with personal values (e.g., sustainability, cultural pride) are highly valued. 42% of UHNWIs have commissioned bespoke fragrances to commemorate special occasions (weddings, milestone birthdays, family gatherings).

Brand heritage and craftsmanship (62%): Established brands with a history of fragrance excellence (e.g., Chanel, Gucci, Hermès) are trusted, but 38% of UHNWIs also seek out niche brands with artisanal production methods (e.g., small-batch blending, handcrafted bottles).

3.2 Purchasing Journey and Channels

The UHNWI perfume purchasing journey is characterized by thorough research, personalized interactions, and a preference for immersive experiences:

Research phase:

Duration: 38% of UHNWIs spend 1–2 months researching perfume purchases, with 27% spending 2+ months for bespoke or high-value limited editions.

Channels: Social media (Instagram, 小红书) is the top research tool (47%), used to discover niche brands, view influencer reviews, and explore scent notes. Luxury lifestyle magazines (e.g., Robb Report Thailand, Tatler Thailand) and private consultations with fragrance experts are also important (35%). 28% of UHNWIs consult with personal stylists or fragrance advisors before purchasing.

Scent testing: 89% of UHNWIs require in-person testing before purchasing, with 64% testing a fragrance for 2–3 days (wearing it in different settings) to assess longevity and sillage. Flagship stores offer "fragrance wardrobing" consultations, where experts recommend 3–5 scents for different occasions and seasons.

Purchasing channels:

Brick-and-mortar flagship stores & bespoke ateliers: 76% of UHNWI perfume purchases occur in physical locations, with private blending sessions (42%) and personal shopping appointments (34%) being the preferred formats. Flagship stores offer exclusive experiences like scent profiling (using AI tools to match preferences), bottle engraving, and access to limited-edition ingredients. For example, Le Labo’s Bangkok atelier offers custom blending sessions where UHNWIs can create unique scents with the brand’s master perfumer, costing 200,000–500,000 Thai baht.

In-resort or in-home shopping: 14% of purchases, particularly for bespoke fragrances and travel-sized collections. Luxury brands like Chanel and Louis Vuitton offer in-villa blending services at top resorts in Phuket and Hua Hin, with average session costs of 150,000 Thai baht.

Digital channels: 10% of purchases, up from 5% in 2023. Direct-to-consumer (DTC) brand websites and luxury e-commerce platforms (e.g., Mytheresa, Farfetch) are used primarily for reordering favorite fragrances or purchasing travel-sized bottles. AI-powered scent recommendation tools (e.g., Byredo’s virtual fragrance advisor) are increasing digital engagement, with 29% of UHNWIs using these tools to discover new scents.

3.3 Gifting Behavior

Perfume is a popular luxury gift among UHNWIs, with distinct gifting patterns:

Gifting frequency: 68% of UHNWIs give perfume as gifts 2–3 times annually, with 23% gifting 4+ times.

Occasions: Weddings (32%), anniversaries (28%), birthdays (21%), and holiday seasons (19%) are the top gifting occasions. Bespoke fragrances are particularly popular for weddings, with 31% of UHNWI couples commissioning custom scents for their wedding day (e.g., bride’s bouquet-inspired fragrance, couple’s signature blend).

Gift preferences: Limited-edition fragrances (45%), bespoke creations (32%), and luxury gift sets (23%) are the top choices. Gift sets often include a full-sized fragrance, travel-sized bottles, and complementary products (e.g., scented candles, body lotion) in matching scents.

Average gift value: 120,000 Thai baht (3,430) per gift, with 18% of gifts exceeding 300,000 Thai baht (8,570) (e.g., bespoke fragrances in crystal bottles, vintage perfume collections).

4. Demographic Variations in Perfume Consumption

4.1 Domestic vs. Foreign UHNWIs

4.1.1 Domestic UHNWIs

香型 preferences: Oriental woody (38%), tropical floral (29%), and cultural Thai ingredients (22%) dominate. 56% prioritize fragrances with Thai cultural resonance, such as lotus or sandalwood-based blends.

Spending patterns: Allocate 40% of perfume budget to domestic luxury brands and bespoke ateliers (e.g., Senada Thai, Oud Thai). Average annual spending: 540,000 Thai baht ($15,400).

Purchasing drivers: Cultural pride (62%), exclusivity (58%), and emotional resonance (55%). More likely to view perfume as a status symbol (47% vs. 32% of foreign UHNWIs).

Preferred channels: Flagship stores in Bangkok (65%) and local bespoke ateliers (25%). Less likely to use digital channels (only 6% of purchases).

4.1.2 Foreign UHNWIs (LTR Visa Holders)

香型 preferences: Niche European woody (35%), clean/sustainable fragrances (28%), and fresh citrus (21%). European expats favor brands like Serge Lutens and Diptyque, while U.S. expats prioritize clean beauty brands like Tata Harper and Credo.

Spending patterns: Allocate 65% of perfume budget to international niche brands. Average annual spending: 650,000 Thai baht ($18,600) – 12% higher than domestic UHNWIs.

Purchasing drivers: Sustainability (78%), scent uniqueness (75%), and convenience (42%). Early adopters of new trends like AI-powered scent profiling (38% vs. 15% of domestic UHNWIs).

Preferred channels: International flagship stores (52%), digital platforms (18%), and in-resort shopping (17%). More likely to purchase travel-sized fragrances (45% vs. 28% of domestic UHNWIs).

4.2 Gender Differences

5. Drivers and Challenges Shaping the UHNWI Perfume Market

5.1 Key Drivers

Economic growth and wealth accumulation: Thailand’s GDP growth of 4.2% in 2025 has increased the number of UHNWIs by 8.5% YoY, expanding the consumer base for ultra-luxury perfume.

LTR visa program: The influx of 7,000+ foreign UHNWIs has added 2.9 billion Thai baht ($83 million) to the UHNWI perfume market, with expats bringing diverse fragrance preferences and higher spending power.

Sustainability trend: The global shift toward purpose-driven luxury has made sustainability a non-negotiable factor for UHNWIs, driving growth for clean and eco-friendly fragrance brands.

Retail infrastructure expansion: The opening of dedicated luxury fragrance spaces (e.g., Central Phuket’s Fragrance Pavilion, Siam Paragon’s Fragrance Hall) has created immersive shopping experiences that cater to UHNWIs’ desire for exclusivity and personalization.

Bespoke perfume trend: The rise of "personal identity luxury" has increased demand for custom fragrances, with ateliers reporting 35% YoY growth in bespoke commissions.

5.2 Key Challenges

Counterfeit products: The Thai perfume market is plagued by counterfeit luxury fragrances, estimated to account for 15% of total sales. 58% of UHNWIs report concerns about purchasing authentic products, particularly online, leading to a preference for in-store purchases.

Sustainability greenwashing: 49% of UHNWIs are skeptical of brands’ sustainability claims, demanding third-party certifications to verify eco-friendly practices. Brands found guilty of greenwashing (e.g., false organic claims) have seen a 25–30% decline in UHNWI sales.

Supply chain disruptions: Limited availability of rare ingredients (e.g., Thai oud, Burmese sandalwood) due to environmental regulations and overharvesting has led to longer waiting lists for high-demand fragrances (average 2–3 months for bespoke blends using rare ingredients).

Changing consumer expectations: UHNWIs are increasingly demanding personalized experiences and unique scents, requiring brands to invest in specialized staff (e.g., master perfumers, fragrance advisors) and custom blending facilities – a costly endeavor for smaller brands.

Climate adaptability: Thailand’s hot and humid climate poses challenges for fragrance longevity and sillage, with 31% of UHNWIs reporting dissatisfaction with how fragrances perform in high temperatures. Brands are responding by developing climate-specific formulations (e.g., lighter concentrations, faster-drying bases).

6. Luxury Fragrance Brand Strategies in Thailand

To cater to the evolving needs of Thai UHNWIs, luxury fragrance brands are implementing targeted strategies focused on exclusivity, sustainability, and personalization:

6.1 Exclusivity and Limited Editions

Thailand-exclusive collections: Brands like Hermès, Dior, and Gucci have launched limited-edition fragrances tailored to Thai culture and preferences. For example, Hermès’ "Lotus du Siam" (2025) blends lotus, jasmine, and sandalwood, while Dior’s "Ayutthaya Heritage" features Thai herb notes. These collections drive 30% higher sales among domestic UHNWIs.

Store-exclusive blends: Niche brands like Le Labo and Byredo offer Bangkok-only scents, available exclusively at their flagship stores. Le Labo’s "Bangkok Santal" (a sandalwood and frangipani blend) has a waiting list of 2 months and commands a 25% premium over the brand’s standard offerings.

Limited-edition packaging: Luxury brands release fragrances in special packaging (e.g., crystal bottles, hand-painted designs) for UHNWIs. Chanel’s 2025 No. 5 "Royal Thai Crystal" edition (limited to 50 bottles) sold out within 48 hours at Siam Paragon, with each bottle priced at 850,000 Thai baht ($24,300).

6.2 Sustainability and Ethical Sourcing

Certifications and transparency: Brands are investing in third-party sustainability certifications and publishing annual ingredient sourcing reports. For example, Stella McCartney Fragrance is certified B Corp and provides detailed reports on the origin and harvesting of organic ingredients.

Sustainable packaging: Luxury brands are adopting eco-friendly packaging, such as recycled glass bottles, biodegradable boxes, and refillable containers. Hermès’ refillable perfume program (launched in 2025) allows UHNWIs to refill their bottles at flagship stores, reducing waste and offering a 15% discount on refills. 42% of UHNWIs have participated in refill programs, with 68% citing sustainability as the key driver.

Ethical ingredient partnerships: Brands are partnering with Thai farmers and cooperatives to source organic, locally grown ingredients. Gucci’s collaboration with northern Thai herb farmers ensures fair wages and sustainable harvesting of lemongrass and holy basil, used in the brand’s "Chiang Mai Herb" collection.

6.3 Personalization and Bespoke Services

Bespoke blending ateliers: Luxury brands are expanding their bespoke offerings, with Le Labo, Byredo, and Chanel opening custom blending studios in Bangkok. These ateliers offer one-on-one sessions with master perfumers, where UHNWIs can create unique scents tailored to their preferences. The process includes scent profiling, ingredient selection, and multiple iterations, with final fragrances presented in custom-engraved bottles. Average cost: 200,000–800,000 Thai baht.

Personalized customer service: Brands assign dedicated fragrance advisors to top UHNWI clients, who remember preferences, recommend new scents, and provide exclusive access to limited editions. For example, Dior’s "Fragrance Concierge" program offers personalized consultations, home delivery, and in-event fragrance services for UHNWI clients.

Customization options: Brands offer a range of customization features, including bottle engraving (names, initials, special messages), custom packaging, and personalized scent notes. Cartier’s "Signature Fragrance" service allows UHNWIs to add a unique note (e.g., a favorite flower or herb) to the brand’s existing fragrances.

7. Conclusion and Future Outlook

Thailand’s UHNWI perfume market is undergoing a profound transformation, driven by shifting values, demographic changes, and retail innovation. In 2025, UHNWIs have redefined perfume as a powerful expression of personal identity, sustainability, and cultural pride, moving beyond mere scent to embrace exclusivity, emotional resonance, and experiential engagement.

7.1 Key Takeaways for Luxury Fragrance Brands

Prioritize exclusivity and uniqueness: Offer Thailand-exclusive collections, store-only blends, and limited editions to cater to UHNWIs’ desire to stand out. Invest in bespoke services, as 34% of UHNWI perfume spending is allocated to custom fragrances.

Embed sustainability authentically: Obtain third-party certifications, use ethical sourcing practices, and adopt sustainable packaging (e.g., refillable bottles) to build trust. Avoid greenwashing, as UHNWIs are highly skeptical of unsubstantiated claims.

Leverage Thai cultural ingredients: Incorporate traditional Thai ingredients (e.g., lotus, lemongrass, oud) into formulations to resonate with domestic UHNWIs. Collaborate with local farmers and artisans to enhance cultural authenticity.

Enhance experiential retail: Design immersive flagship stores with scent libraries, blending stations, and personalized services. Host exclusive events and offer in-resort/in-home experiences to deepen customer relationships.

Tailor to demographic differences: Customize offerings for domestic vs. foreign UHNWIs, men vs. women, and different age segments. For example, offer niche European brands for foreign expats and cultural blends for domestic UHNWIs.

7.2 Future Trends (2026–2030)

Sustainable luxury mainstreaming: Sustainability will become the top purchasing factor for UHNWIs, with 85% expected to prioritize eco-friendly fragrances by 2028. Brands that fail to meet strict sustainability standards will lose market share. The sustainable fragrance segment is projected to grow at 45% YoY through 2030.

Tech-integrated personalization: AI and blockchain will revolutionize perfume consumption, with AI-powered scent profiling (matching preferences to ingredients) and blockchain-verified ingredient sourcing becoming standard. Virtual reality (VR) fragrance testing (allowing UHNWIs to "experience" scents digitally) will gain traction, particularly among younger UHNWIs.

Bespoke perfume expansion: The bespoke segment will grow at 38% YoY, with more brands opening custom blending ateliers in Bangkok and Phuket. "Fragrance wardrobing" (curating 5–10 custom scents for different occasions) will become a status symbol among UHNWIs.

Cultural fusion fragrances: International brands will increasingly collaborate with Thai artisans and farmers to create fusion fragrances that blend global luxury with local culture. These fragrances will appeal to both domestic and foreign UHNWIs, driving cross-cultural consumption.

Wellness-focused fragrances: The intersection of perfume and wellness will expand, with brands launching fragrances infused with aromatherapy benefits (e.g., stress-relief, sleep enhancement). These fragrances will align with UHNWIs’ focus on longevity and holistic wellness, growing at 32% YoY through 2030.

In conclusion, Thailand’s UHNWI perfume market is poised for exceptional growth, with brands that can adapt to evolving values of exclusivity, sustainability, and personalization well-positioned to thrive. By understanding the nuanced preferences and behaviors of this cohort, luxury fragrance brands can build long-term relationships with Thai UHNWIs and capitalize on the country’s status as a leading luxury hub in Southeast Asia.